Delmar Jewelers is a global jewelry designer and manufacturer working with retailers across North America. This report analyzes Delmar’s internal order data from the past two holiday seasons to examine shifts in consumer purchasing behavior, including changes in shopping timing, pricing, and product preferences, with a focus on the 2025 holiday period.

Timeframe

Black Friday remained the strongest sales period in both 2024 and 2025, but Cyber Week played a significantly larger role in 2025. Higher Cyber Monday order volumes point to increased consumer responsiveness to promotions, suggesting that Cyber Week functioned as an extended shopping window rather than a single peak moment.

Beyond Cyber Week, purchasing activity in 2025 shifted noticeably earlier in the holiday season. Compared to 2024, which saw a higher concentration of last-minute December shoppers, a larger share of orders in 2025 was placed between September and November, indicating that consumers are spreading holiday spending across earlier periods rather than concentrating it at year-end. This pattern mirrors a broader trend observed across other retail categories in the market (MetricsCart, 2026).

In 2025, Delmar Jewelers has seen people shopping earlier in the season, a trend that has become clearer over time. This shift resulted in fewer last-minute purchases and a more evenly distributed sales pattern throughout the holiday cycle.

Timeframe (Click image for larger view)

Time of Day

In Delmar’s analysis, order activity was highest during midday hours, with most purchases placed between 11:00 a.m. and 3:00 p.m., peaking at 2:00 p.m. This pattern is consistent with broader U.S. e-commerce research, which has found that online shopping activity often increases around lunchtime and early afternoon, when consumers tend to browse and complete purchases during workday breaks (Oberlo, n.d.).

Time of Day (Click to view larger image)

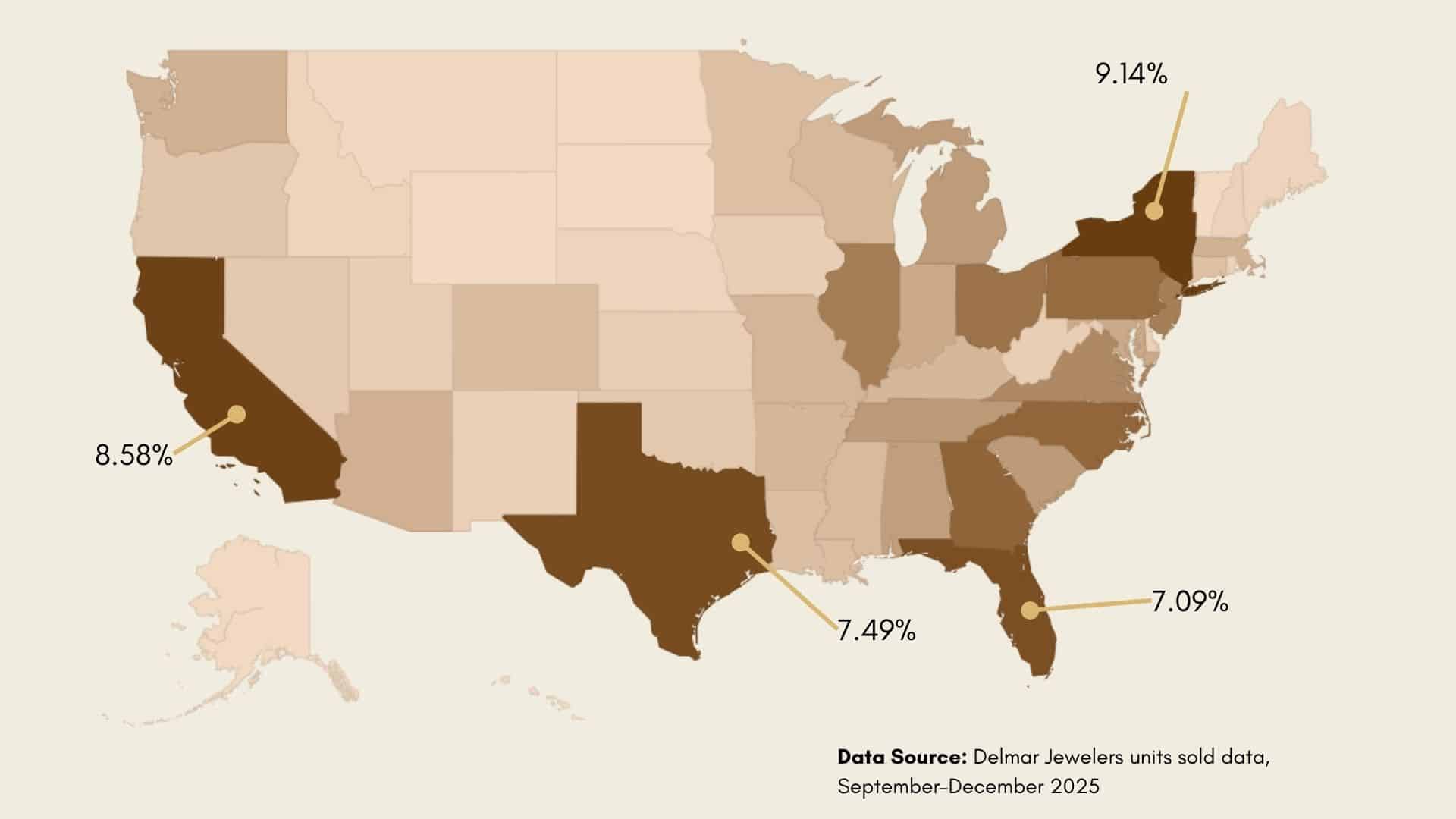

2025 State Overview

Based on Delmar’s internal sales data from September through December 2025, New York recorded the highest volume of jewelry purchases during the holiday season. California, Texas, and Florida followed as the next strongest states by quantity sold. Together, these four states accounted for over 30% of total holiday order volume.

We’ve noted that the outer states continue to be the most fashion-oriented, with a higher concentration of trend awareness, and jewelry sales being significantly stronger in these markets.

2025 State Overview (Click to view larger image)

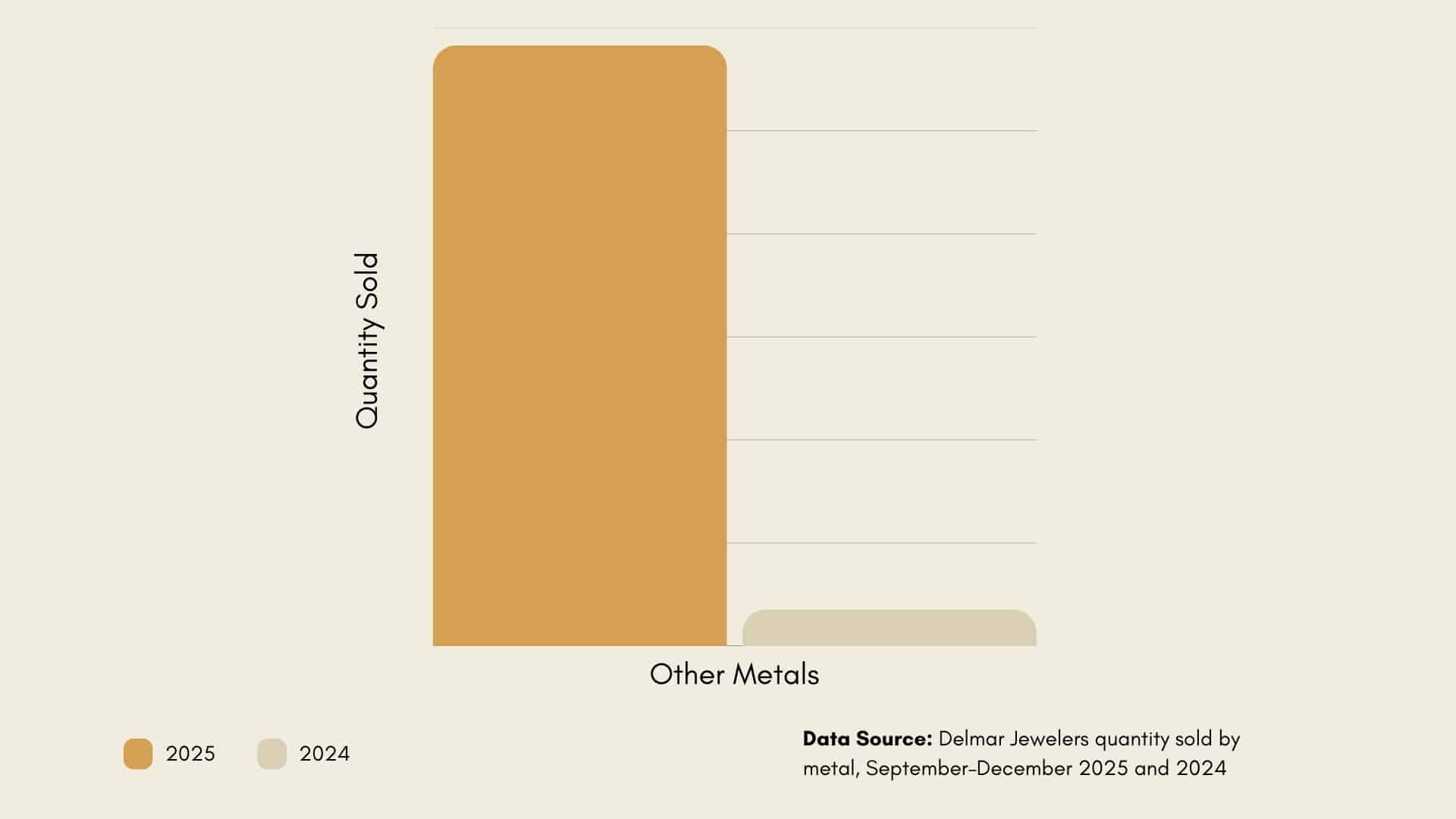

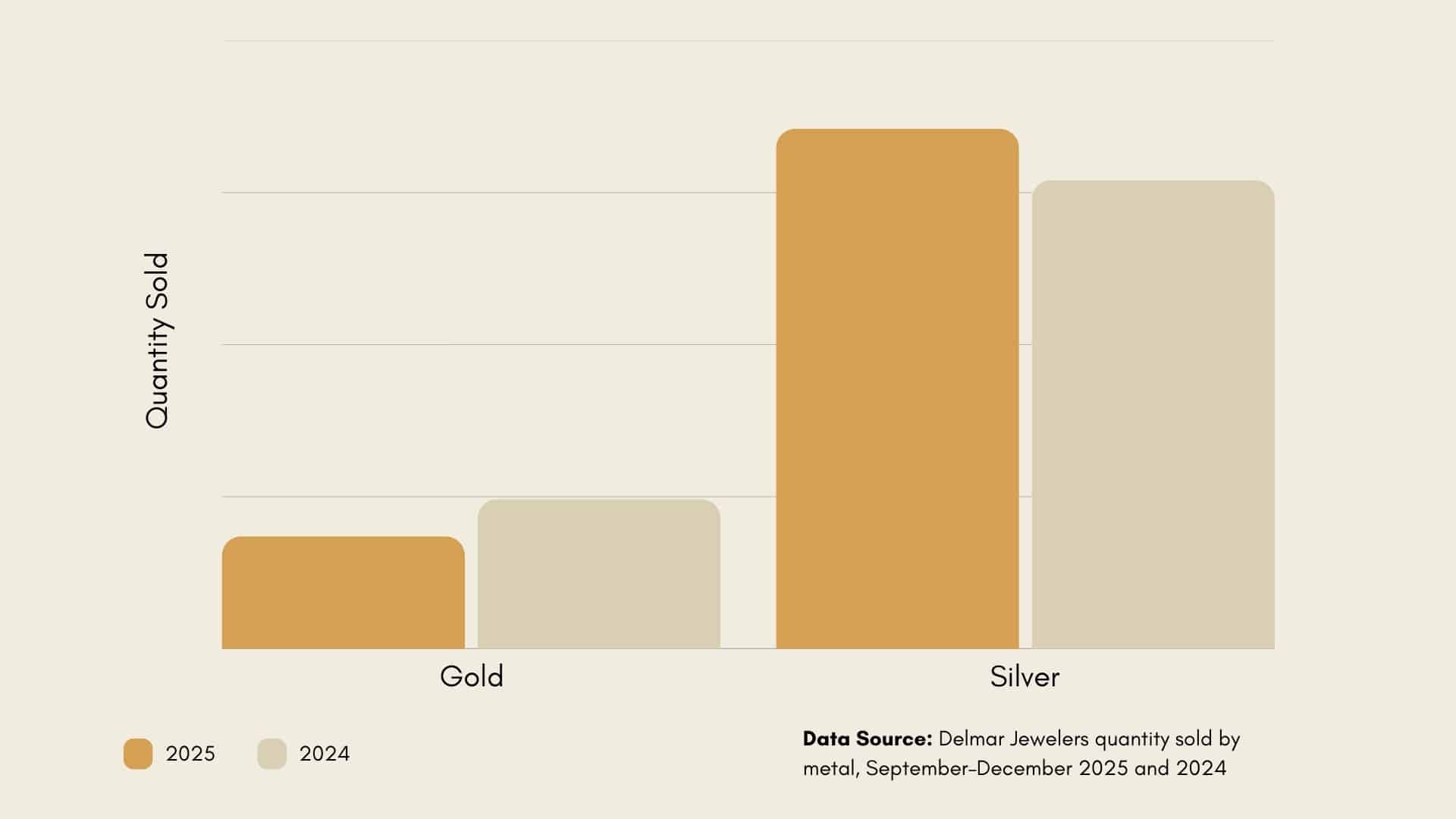

Metal Overview

Overall, gold jewelry accounted for a smaller share of holiday unit sales compared with the 2024 season, while silver and alternative metals such as brass and stainless steel saw a sharp increase in volume. This shift is consistent with rising gold prices, which may be influencing consumer preferences toward more affordable materials.

Other Metals (Click to view larger image)

Gold and Silver (Click to view larger image)

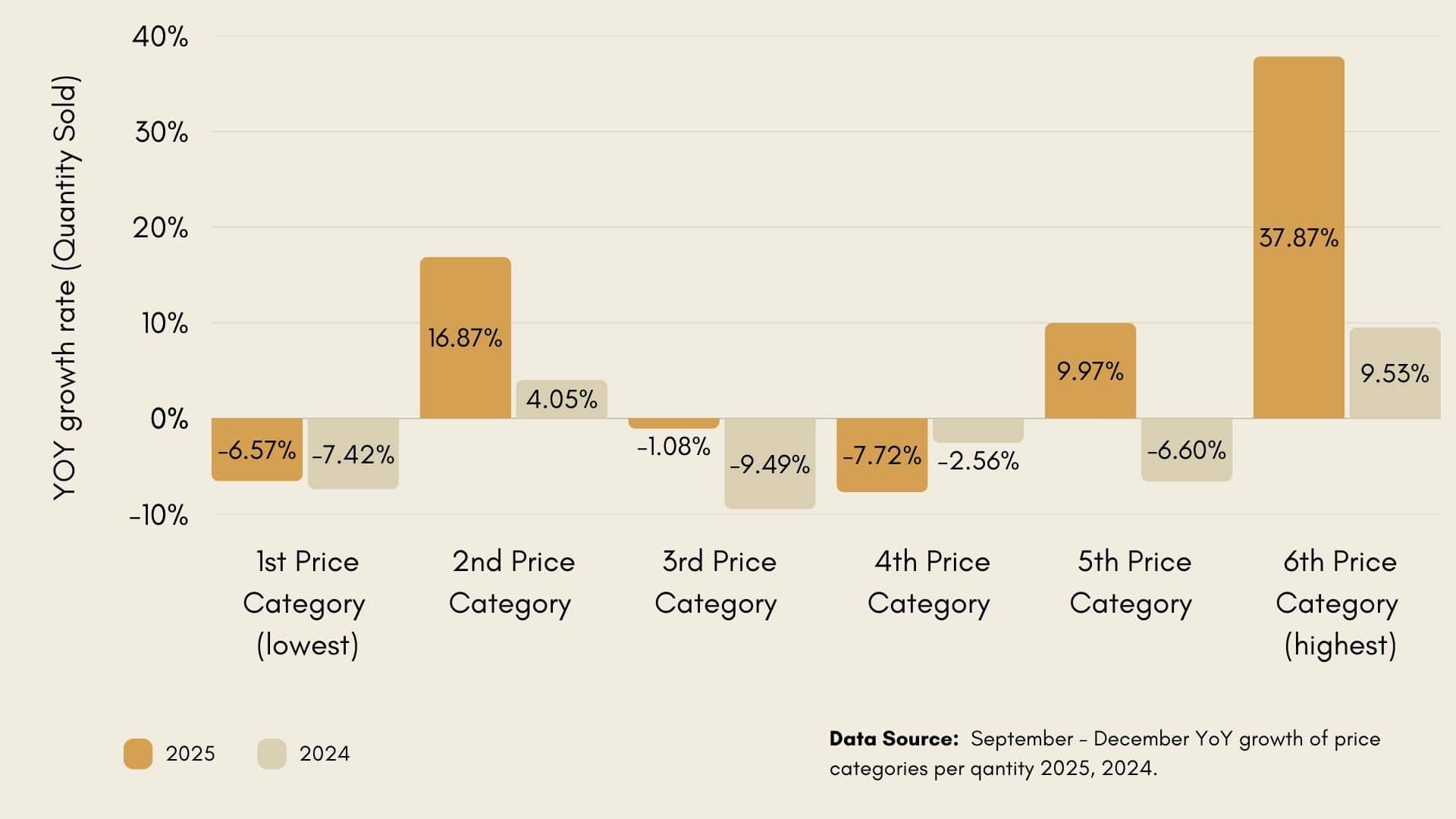

Price Category

Looking at approximate retail prices between September and December 2025, a larger share of order volume shifted toward higher price categories. Compared with prior periods, fewer purchases originated in the lowest price tier, with demand moving into the second-lowest category and away from the middle price tiers.

With metal prices continuing to rise, we are seeing consumers trade up rather than buy more. Shoppers today are aiming for higher price categories and investment-focused pieces, which is driving a shift away from the lowest tiers toward higher-value items. This behavior is not unique to Delmar’s customer base but can be observed across the U.S. jewelry market more broadly (Tenoris, 2026).

The strongest growth occurred in the highest price category, which recorded a 37.87% increase in units sold compared with the same period in 2024. While this segment had already grown during the 2024 holiday season (+9.53% year over year), the acceleration in 2025 points to a more pronounced shift in purchasing behavior. Overall, the data suggests that consumers are buying fewer items but spending more per piece, reflecting a growing emphasis on quality, longevity, and higher-value jewelry purchases.

Price Category (Click to view larger image)

Lab-Grown Diamonds

Lab-grown diamonds were the fastest-growing category during the period analyzed. In 2024, sales in this category increased by 699% compared with 2023, followed by a further 117% growth in units sold between 2024 and 2025.

While part of this acceleration reflects a smaller starting base, the sustained year-over-year expansion points to rapidly increasing adoption and demand. Market research suggests this momentum is likely to continue, with the U.S. lab-grown diamond market projected to grow further in the coming years as consumer acceptance and product availability expand (Morgan, 2025).

Lab-Grown Diamonds (Click to view larger image)

Conclusion

Lab-grown diamonds were the fastest-growing category The 2025 holiday season highlights a continued shift in how consumers approach jewelry purchases, with spending spreading earlier across the season, greater responsiveness to extended promotional periods, and a clear move toward higher-value pieces. Rather than buying more, shoppers increasingly prioritized quality, longevity, and perceived investment value, influencing trends across metals, price categories, and emerging segments such as lab-grown diamonds.

What we’re seeing is a more deliberate consumer. Shoppers are planning earlier, trading up, and focusing on pieces that feel meaningful and lasting rather than purely transactional. Together, these patterns suggest that future holiday success will depend less on last-minute demand spikes and more on aligning assortments, pricing, and promotions with an increasingly intentional and value-driven customer.